The State of the Second Hand HDD Rig Market

By Bob Martin - General Manager - May 31, 2012

AS PUBLISHED IN TRENCHLESS WORLD

JUNE 2012

It has been a challenging few years. Contractors, manufacturers, resellers and most everyone in general saw a reduction in spending, a loss of jobs and an overall loss of income as a result of the global recession that hit in late 2008.

Obviously, this environment changed the way that contractors conducted business. While jobs still needed to be bid and completed, the amount of money available to support those jobs saw a large reduction. As such, there was a noticeable migration of interest from new equipment purchases to used equipment purchases.

Used Equipment Availability

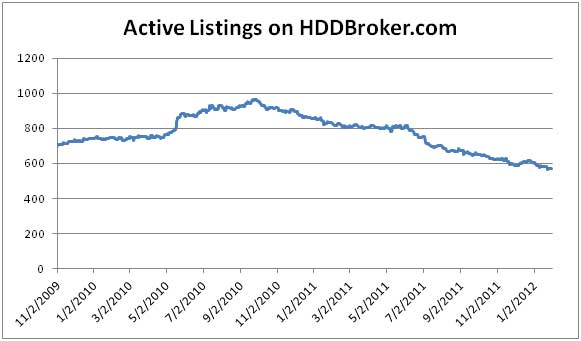

If we first take a look at the amount of inventory available on the used HDD marketplace, we can begin to see a relationship between the state of the economy and the availability of used equipment.

If we use the beginning of 2009 as the effective beginning of the global downturn, we can see that, for the most part, contractors gritted their teeth and continued with business as usual in hopes of riding out the storm. This tendency continued through to the beginning of summer in 2010 when the recession gloom did not seem to have an end in sight.

At that point, we saw a marked increase in the number of used equipment listings. It could be assumed that equipment owners at that point began a calculated liquidation of non-vital assets in order to preserve cash flow and remain solvent.

It is interesting to note at this point that this strategy of strategic liquidation is a much different outcome of the downturn than the outcome of the huge industry crash of 2001 that saw a huge percentage of the HDD contractors bankrupt and their equipment seized by the banks and lending institutions that financed them. During that period, we saw a very large number of instances of company bankruptcies. The wondrous wave of seemingly limitless money had passed and companies suddenly found themselves with millions of dollars worth of equipment with no work for them.

This period saw mass liquidation of HDD equipment through brokers and auction sites at the barest fraction of the equipment's previous values. International buyers unaffected by the domestic hardships bought this cheap, high quality equipment by the container full while US contractors folded their companies and turned their efforts into rebuilding their means of income in other, less volatile markets.

Many of the US companies during this time chose to hang onto their equipment until there was no other option and bankruptcy was forced upon them. Valuable lessons were learned in regards to identifying changes in the market and strategies to help offset the fallout.

Conversely, the global recession saw a much different overall strategy adapted. Much of this may have to do with the more gradual decline in work and pricing. The 2001 downturn occurred very nearly overnight and offered little in the way of opportunity for strategic thinking about loss mitigation. The global recession of 2008, however, saw a gradual decline over years. As such, contractors were allowed time to strategically liquidate equipment that was not integral to the operations of the company, preserving their viability to continue forward. Instances of bankruptcy and the volumes of bank repossessions were comparatively miniscule compared to the previous downturn.

Moving forward to the end of 2010, we can now see the peak of the used equipment inventory. It is fair to assume that it was around this time that people realized that regardless of the state of the global economy, jobs needed to be bid, work still needed to be carried out, and the equipment for these installations purchased. Of course, the amount of work was comparatively small, the money being offered for the jobs much less, and the cash on hand for purchases a small fraction of previous years.

This is where the used market really began to see demand. A steady, strong demand for quality used HDD equipment began to manifest as contractors turned to the used marketplace as an alternative to new equipment offerings. Demand began to outstrip supply, and the overall inventory of used equipment began a steady decline.

Another major factor in this equation also has to do with the downturn of 2001.

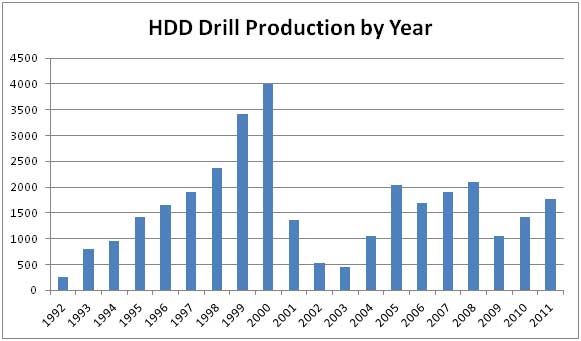

Traditionally, the highest demand for used equipment falls at the seven to ten year range from the manufacture date. For example, the highest demand during 2008 was for equipment manufactured between 2001 and 1998. Equipment at this stage of its life has typically seen the greatest amount of depreciation and yet still has a high degree of productivity.

Unfortunately, looking back seven to ten years from 2011 puts us in the 2001 through 2004 range. As a result of the US downturn, all of the major HDD manufacturers saw enormously decreased production of HDD drills from 2002 through 2004.

You can see in the above chart that 2002 and 2003 saw production numbers approximately one tenth that of 2000. With very few new rigs entering the market in those years, we see a conservatively estimated loss of over six thousand used HDD drills if we were to use an average of 2500 units manufactured per year as the baseline required for a steady used marketplace. That is a huge number and certainly a good contributor to why availability on the used market is an issue at this point.

What is Selling?

I would like to preface this next section by saying that the data presented in the following charts is by no means a comprehensive survey of the entire used equipment marketplace. The information in the following section is gleaned from the sales history of HDD Broker LLC, and while it will admittedly not be one hundred percent accurate, is should be a sufficiently large cross section to offer some valuable insight into the used equipment marketplace.

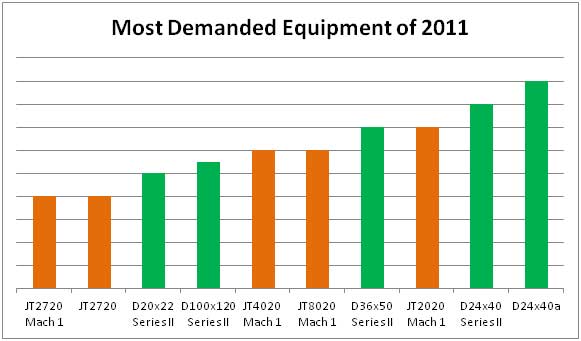

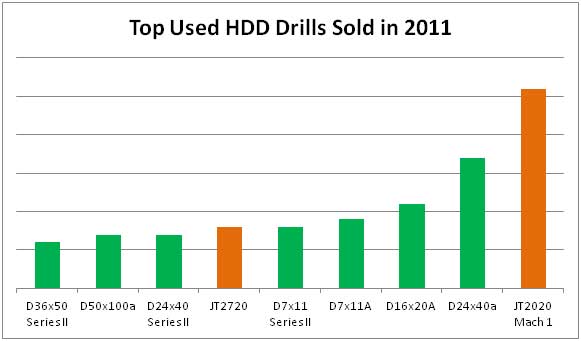

Looking at the first two charts, we can see some parallels between what people are inquiring about and what they are actually purchasing at the end of the process. The venerable Vermeer D24x40A remains a high-demand machine. It has seen a successful run since its inception back in 1997. The success of that platform has carried over to its successor, the D24x40 Series 2. Those machines are high in both demand and successful closed sales.

The Ditch Witch JT2020 Mach1 drill platform has seen considerable success in the used marketplace, and there is a very good reason. In the 20,000lb pullback size range we can see that the two top contenders are the 2020 Mach 1 and the Vermeer D20x22 Series 2. The Ditch Witch offering was first seen in 2004, and that introduction went very well. The machine has seen very few changes over the years and continues to be a productive drill to this day. Vermeer's offering, on the other hand, was released in 2008. Its predecessors included the D18x22 and the D20x22 Series 1 drills. Both of those models saw limited traction in the industry, which left Ditch Witch a wide open playing field to fill with their offering.

If you recall, it was mentioned earlier that demand on the market usually follows a machine by approximately seven years. With that being the case, it makes perfect sense for the JT2020 to have a good market share in the used industry, one that may continue until the newer Vermeer offering depreciates enough to compete on a pricing basis.

There are good examples older equipment models placing in the top levels of sales. Most of the new generation of drills emerged in the 2006 and later years. Looking forward to the same demand formula we've established above, it should be in the next few years that the new generation begins to slowly push the older models from the upper levels of these charts.

Also note that we have seen a couple of larger drill models see their way into the top equipment that is being inquired after. The Ditch Witch JT8020Mach 1 and the Vermeer D100x120 Series 2 drills both see considerable interest, however if you look at the top drills actually sold, they do not place. This may indicate a desire on behalf of contractors to explore or quote larger jobs, but a lack of actual contracts or financial means to follow through with the purchase.

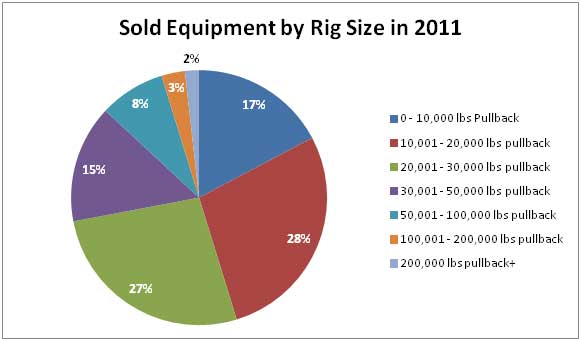

The majority of the units sold in 2011 fall squarely in the 10,000 to 30,000lb size range. This is certainly of no surprise as most of the jobs out there revolve around utility installation and those units have probably the highest degree of flexibility and cross many different industries. All of the top selling units in the above chart except for the D50x100A fall into this size range, giving solid reinforcement to the data.

In the next article, we will touch on the latest used equipment trends that actually show a recent and steady increase in used equipment inventory, and also just what the burgeoning new equipment sales are doing to used equipment sales.

The use of trademarked names herein does not suggest sponsorship or association of the author with the trademark owner's product or service. All trademarked names are the exclusive property of their respective owners.

This commentary is presented for informational purposes only. It is not intended to be a comprehensive or detailed statement on any subject and no representations or warranties, express or implied, are made as to its accuracy, timeliness or completeness. Nothing in this commentary is intended to provide financial, legal, accounting or tax advice nor should it be relied upon. Neither HDD Broker LLC nor the author is liable whatsoever for any loss or damage caused by, or resulting from, any use of or any inaccuracies, errors or omissions in the information provided.